What is Dwelling Fire Insurance & When do I need it?

- Your Good Insurance Agency

- June 16, 2022

- 12:48 pm

When you live in California, it can be hard to obtain the homeowners insurance you need due to wildfires and other risk factors that come with living in this beautiful state. Luckily, almost all homeowners and renters are eligible for dwelling fire coverage.

Unfortunately, there isn’t a whole lot of great information out there to help you answer questions like, “What does a dwelling fire insurance plan cover?” and “Will a dwelling fire companion policy give me the coverage I need to protect my home for years to come?” However, as one of the leading providers of dwelling fire policies in San Diego, Your Good Insurance is here to help you understand everything there is to know about dwelling fire insurance so you can determine what policy is right for your home.

What Is Dwelling Fire Insurance?

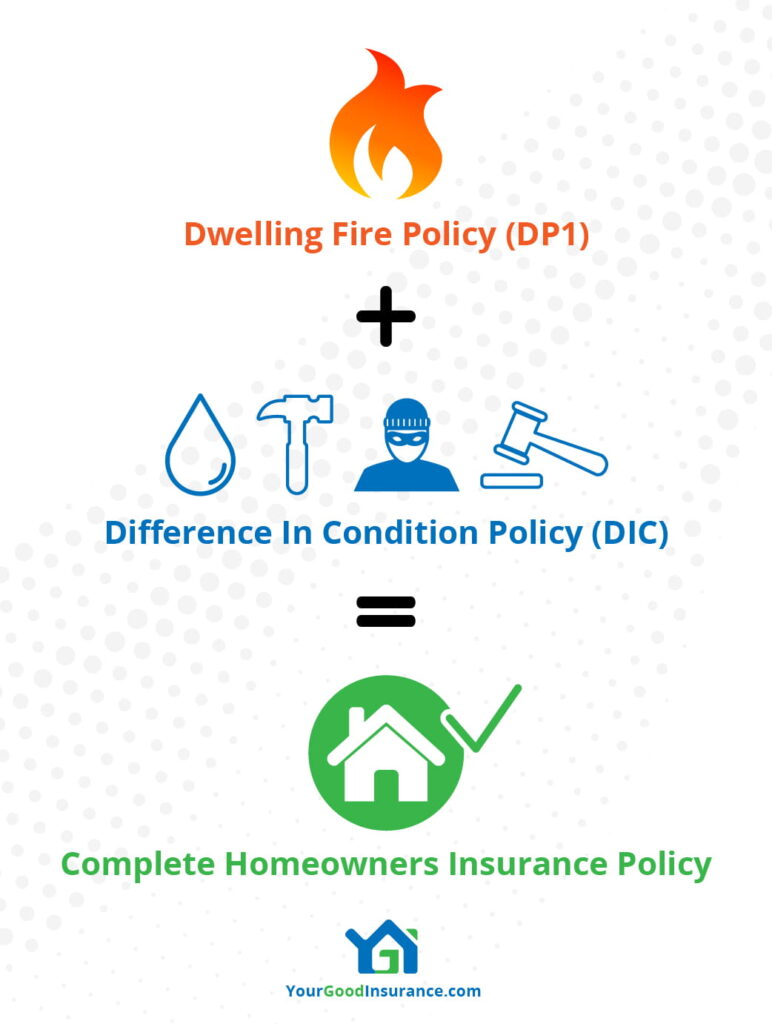

A dwelling fire insurance policy is considered a “bare bones” insurance plan, also known as basic property insurance or a named peril policy. These plans can cover standard homes between 500 to 10,000+ sq ft.

Your home can be insured at either replacement cost or extended replacement cost, and you can also add on a dwelling fire companion policy (DIC – Difference in Conditions) to provide additional coverage for other perils including sudden and accidental discharge of water, theft, and liability.

Dwelling Fire Insurance policies are usually obtained through insurance brokers. Your Good Insurance can help you determine the best coverage options, including your dwelling fire companion policy.

The Purpose of Dwelling Fire Policies

When insurance companies determine coverage for your home or other property, they evaluate the location risk. This risk assessment is based on the home’s condition, and other data about the neighborhood you live in. Nowadays, many homes in California lie in a wildfire zone. For this reason, many insurance providers won’t even offer home insurance in wildfire zones.

This is why dwelling fire policies exist — they provide coverage to homeowners who would otherwise be denied homeowners insurance. These plans make sure you can protect one of your most valuable investments: your home.

What Does a Dwelling Fire Policy Cover?

A Dwelling Fire Policy can offer wildfire insurance options for a wide variety of homes, including:

- Owner-occupied units (traditional homes)

- Seasonal rental homes that are rented out for part of the year

- Rental property that the homeowner rents out to tenants (also called landlord insurance)

- Condominium units

Furthermore, manufactured homes near brush can be insured with a dwelling fire plan, but only for actual cash value.

Dwelling fire policies will provide coverage regardless of location, meaning your home can receive a policy even if you live in California wildfire zones or have been previously denied because you need brush insurance due to your home’s proximity to brush and other fire hazards.

Note: A dwelling fire policy is a great option for people who live in notable high-risk zones, such as Escondido, where brush fires are frequent. If you’re concerned about brush fire in Escondido, Your Good Insurance Agency can help you find the right insurance policy to meet your needs.

What Does a Dwelling Fire Policy Cover For Your Home?

Like most other types of homeowner policies, a dwelling fire policy covers your dwelling (the home itself) and additional structures on the property such as a garage, porch, shed, or fence. Additionally, this insurance policy provides personal property coverage for any items such as clothing, furniture, and electronics inside your home.

Note: Most dwelling fire policies cover actual cash value (ACV) or replacement cost of any personal property damaged or lost due to the perils listed on the policy. Make sure to consult with your agent at Your Good Insurance to get the coverage that suits your needs.

Unlike most standard homeowners insurance policies, dwelling fire policies are named peril policies, meaning they only provide coverage for specific types of damage listed directly in the policy. Because dwelling fire policies are essentially home insurance in wildfire zones they cover primarily fire claims. Additionally, there are extended coverages available that cover a few other perils.

More specifically, a dwelling fire policy generally covers damage directly caused by:

- Fire

- Lightning

- Smoke

- Internal explosion

- Vandalism and malicious mischief (with an endorsement)

- Extended coverage: windstorm or hail, explosion, riot, aircraft, vehicles (with an endorsment)

For all other types of coverage, homeowners will need to purchase a Difference in Conditions policy (DIC) as part of a dwelling fire companion policy.

Also, many dwelling fire policies (DP1) have a cap as to how much value it will cover for your home. This coverage includes Personal Property, other structures, Fair Rental Value, Ordinance and Law, Debris Removal, Fences, and Plant Shrubs and Trees.

Dwelling Fire Insurance And DIC Coverage

Because your home is one of your most important and most expensive possessions, you will want to make sure you have adequate coverage in case of any type of disaster, not just wildfire insurance or brush insurance through your dwelling fire policy. In most cases, people add more complete property coverage through a Difference in Conditions, or wrap-around policy.

If you’re asking yourself, “What is a DIC insurance policy?” don’t worry. Most people are unfamiliar with the term. Essentially, DIC insurance is a specific type of insurance coverage that is typically paired with a dwelling fire policy to add coverage for additional perils that are not listed within the dwelling fire policy. Although it costs an additional fee, it is well worth the investment for your peace of mind as well as to meet mortgage lender requirements.

Typically, DIC insurance adds on these additional types of coverage to provide a wrap-around, or more complete, coverage to your home. This means that it adds on coverage to your dwelling, outbuildings and personal property for other listed perils.

In most cases, a DIC plan will provide coverage for:

- Sudden and accidental discharge of water

- Theft of your personal property

- Personal liability

- Loss of Use (as long as it’s for a claim covered by the DIC)

Additionally, you can add endorsements to provide replacement cost values for your home and possessions instead of actual cash value, and you can add additional coverage for landscaping or other items located on your property. These are all valuable coverage offerings that come as part of a standard homeowners policy but are not included in a dwelling fire plan due to the elevated risk.

Together, a dwelling fire policy and DIC coverage provide a close equivalent to a traditional homeowners policy for anyone who lives in California wildfire zones.

Note: Earthquake coverage is another add-on policy you may need.

When Do I Need Dwelling Fire and DIC Insurance?

Dwelling fire policies can give California residents a chance to obtain homeowners insurance even when most companies were unwilling to cover the home. There are certain criteria for writing a dwelling fire policy but most homes in decent shape will have no problem qualifying.

Most of the time, insurance providers use Public Protection Classes (PPC) to determine your home’s perceived risk. This rating system works on a 10 point scale, with 10 being the highest risk home. Those with a score of 9 or 10 typically do not qualify for a traditional homeowners policy based on the perceived risk of fire hazard associated with their home. These homes often fall into areas known as California wildfire zones or may have additional risks that would make them harder to save in the event of a wildfire in the area.

In addition to the enhanced risk factors that make you ineligible for other types of insurance, dwelling fire policies can only be issued to applicants whose homes meet the mandated building requirements.

Rating Factors for Dwelling Fire Insurance

Although dwelling fire policies can be designed to help individuals obtain homeowners insurance even when they live in California wildfire zones or other high-risk areas, insurance underwriters still use certain rating factors to determine coverage and premium totals. While this doesn’t necessarily mean your home will not qualify for a dwelling fire policy, it does mean that you may be assessed additional fees or need to take additional steps to obtain coverage.

Some rating factors for dwelling fire plans include:

- The home’s age

- Property location

- Proximity to fire station

- Access to public water (public water can include a public fire hydrant but not a well)

- Claim history

- Chosen coverage and deductible amounts

Note: If your home water supply is provided by a well, you can still get insurance through dwelling fire policy. However, your rates will likely be higher and your well will need to have a 10,000 gallon reserve with a fire hose hookup.

Let Your Good Insurance Agency Help You Navigate Dwelling Fire Policies

Getting a dwelling fire policy doesn’t mean you’re out of options — it’s just a specific type of homeowners policy for people who live in high-risk areas. Every homeowner is entitled to their own preferences about how their Dwelling Fire Policy is written and what additional coverages they want to add into their DIC insurance. So whether you are insuring a vacation home or your dream house, Your Good Insurance Agency is here to help.

Your Good Insurance is a leading provider of dwelling fire policies in San Diego. We offer great dwelling fire and DIC insurance options to meet virtually any family’s needs. We can help you find the coverage you need, even if you live near brush or in a high-risk region. Call us so we can help you sculpt your coverages to meet your particular set of needs. We want to help you find that calming peace of mind that comes with knowing your most valuable possession is secured with the best possible coverage.

Insurance Made Easy

Get A Quote Now

As a broker we will price this with up to 30 carriers to get you the absolute best price.